Is Money Available For Usda Loans Nov 2018 Cr

USDA home loans: USDA loan requirements & rates for 2022

January 26, 2022

-

21 min read

What is a USDA dwelling loan?

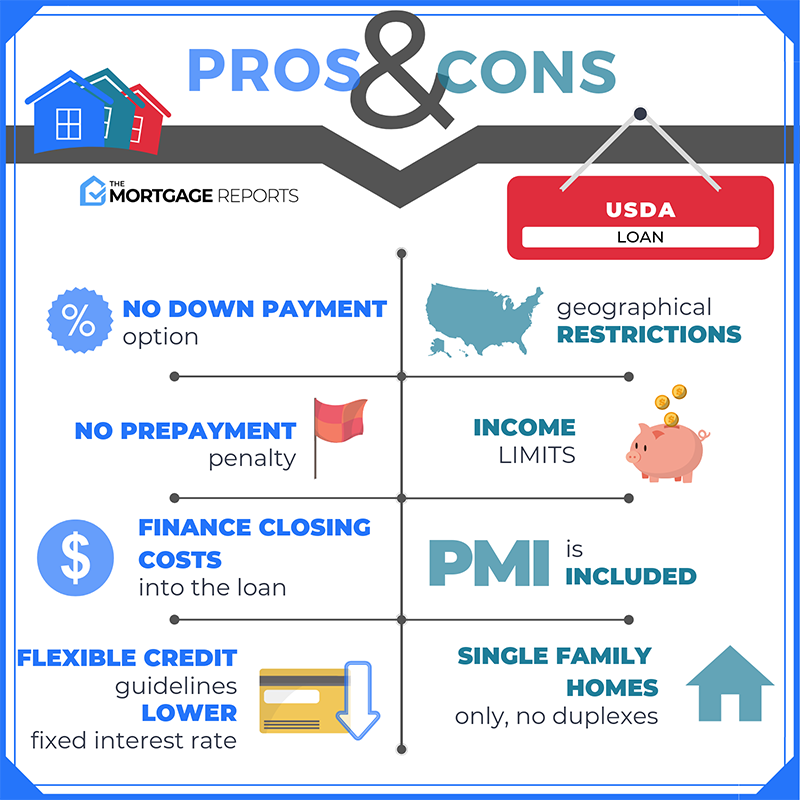

USDA loans are mortgages backed by the U.Southward. Department of Agriculture as function of its Rural Development Guaranteed Housing Loan program.

USDA loans are available to home buyers with low-to-boilerplate income. They offer financing with no down payment, reduced mortgage insurance, and below-market mortgage rates.

Y'all tin use a USDA mortgage to purchase a home or refinance one you lot already own at a low rate.

In short, USDA home loans are putting people in homes who never thought they could exercise anything only rent.

In this article (Skip to…)

- USDA loan requirements

- USDA loan rates

- How USDA loans work

- USDA loan mortgage insurance

- About USDA loans

- FAQ

>Related: How to buy a house with $0 down: First-time home buyer

USDA loan requirements

USDA loan requirements are based on the buyer and the belongings.

First, the home must be in an eligible rural surface area, which USDA typically defines every bit a population of less than 20,000.

Second, the buyer must meet USDA monthly income caps. To be eligible, y'all tin can't make more than 15% higher up the local median income. You as well have to use the home equally your main residence (no vacation homes or investment properties immune).

Finally, borrowers have to meet the lender's bones financial requirements, including:

- Income eligibility: Steady task and monthly income, proven past tax returns

- Credit requirements: FICO credit score of at least 640 (though this can vary by lender)

- Existing debt ratio: Debt-to-income ratio of 41% or less in most cases

To observe out if the property you're buying is a USDA eligible rural area and if you lot come across local income limits, you can utilise the USDA's eligibility maps.

USDA loan rates: How do they compare to FHA & conventional?

Compared to other dwelling loan programs, USDA mortgage involvement rates are some of the everyman bachelor.

USDA rates are typically only matched by the VA loan, which is exclusively for veterans. These two programs — USDA and VA — can offer below-market place involvement rates because their government guarantee protects lenders against loss.

Other mortgage programs, like the FHA loan and conventional loan, tin can have rates effectually 0.5%-0.75% higher than USDA rates on average.

That said, mortgage rates are personal. Getting a USDA loan doesn't necessarily mean your charge per unit volition be "below-market" or lucifer USDA loan rates advertised.

To get the everyman possible rate and monthly payments, you lot need an excellent credit score and a depression debt-to-income ratio. Making a bigger down payment helps, too.

Y'all too need to shop around with a few dissimilar USDA mortgage lenders.

Each USDA lender sets rates differently — so comparing personalized rates from more than than one company is the but style to find your lowest option.

How USDA loans work

Using a USDA loan, buyers can finance 100% of a home purchase cost while getting admission to better-than-boilerplate mortgage rates. This is because USDA mortgage rates are discounted every bit compared to other low-down payment loans.

Beyond that, USDA loans aren't all that different from other home loan programs.

The repayment schedule doesn't feature a "balloon" or annihilation non-standard; the closing costs are ordinary; and, prepayment penalties never use.

The ii areas where USDA loans are different is with respect to the loan type and down payment amount.

- With a USDA loan, you don't have to make a down payment. This is one of only two major loan programs that allow zero-downward financing

- The USDA loan plan requires you to take a fixed-rate loan. Adjustable-rate mortgages are not available via the USDA rural loan program

Rural loans can be used by first-time home buyers and echo home buyers alike. Homeowner counseling is not required to utilise the USDA program.

USDA loans require mortgage insurance (MI)

USDA guarantees its mortgage loans, meaning it offers protection to mortgage lenders in instance USDA borrowers default. Simply the plan is partially self-funded.

To keep this loan program running, the USDA charges homeowner-paid mortgage insurance premiums.

As of October 1, 2016, USDA has lowered its mortgage insurance costs for both the upfront and annual guarantee fees.

The electric current USDA mortgage insurance rates are:

- For purchases: i.00% upfront guarantee fee, based on the loan corporeality

- For refinancing: i.00% upfront guarantee fee, based on the loan corporeality

- For all loans: 0.35% annual guarantee fee, based on the remaining principal balance each year

As a real-life example: A home heir-apparent with a $100,000 loan size would take a $one,000 upfront mortgage insurance cost, plus a monthly payment of $29.17 for the annual mortgage insurance.

USDA upfront mortgage insurance is non paid as cash. It's added to your loan balance for you lot, so you pay it over fourth dimension.

USDA mortgage insurance rates are lower than those for conventional or FHA loans.

- FHA mortgage insurance premiums include a 1.75% upfront mortgage insurance premium, and 0.85% in MIP annually

- Conventional loan private mortgage insurance (PMI) premiums vary based on your DTI, credit scores, and additional factors, simply they can tin can achieve above 1% annually

With USDA-guaranteed loans, mortgage insurance premiums are just a fraction of what you'd typically pay. Even better, USDA mortgage rates are low.

USDA mortgage rates are frequently the lowest among FHA mortgage rates, VA mortgage rates, and conventional loan mortgage rates — particularly when buyers are making a small or minimum down payment.

For a heir-apparent with an average credit score, USDA mortgage rates tin be 100 basis points (1.00%) or more below the rates of a comparable conventional loan.

Lower rates mean lower mortgage payments each month, which is why USDA loans can exist extremely affordable.

Nearly the USDA Rural Housing Mortgage

The Rural Development loan'southward full name is the USDA Unmarried Family unit Housing Guaranteed Loan Program. However, the program is more normally known every bit a USDA loan.

The Rural Development loan is sometimes chosen a "Section 502" loan, which refers to section 502(h) of the Housing Act of 1949, which makes the program possible.

This programme is designed to help single-family home buyers and stimulate growth in less-populated, "rural," and low-income areas.

That might audio restrictive. Merely in fact, 97% of the U.S. map is eligible for USDA loans, including many suburban areas virtually major cities. Any area with a population of twenty,000 or less (or 35,000 or less in special cases) can be an eligible rural area.

Yet most U.South. home buyers, even those who have USDA loan eligibility, haven't heard of this program or know picayune nigh it.

This is because the USDA loan program wasn't launched until the 1990s. Only recently has it been updated and adjusted to appeal to rural and suburban buyers nationwide.

Many USDA-canonical lenders don't even list the USDA loan on their loan application menu. But many offering information technology.

So if y'all think y'all're eligible for a zero-downwardly USDA loan, it's worth asking your shortlist of lenders whether they offer this program.

USDA home loan FAQ

What is a USDA loan?

USDA loans are special mortgages meant for low- to moderate-income home buyers. These loans are guaranteed by the United States Department of Agriculture. That guarantee acts equally a form of insurance protecting USDA lenders, so they're able to offering below-marketplace involvement rates and null-down home loans. USDA runs this program to encourage homeownership for low-income families and economic development in rural areas.

How practise yous qualify for a USDA loan?

You might qualify for a USDA loan if you have an average salary for your area and a credit score of 640 or higher. USDA loans tin be used to buy a home but in a rural or suburban area. Typically, qualifying areas take a population nether twenty,000.

What is the income limit for USDA home loans?

The income limit for USDA domicile loans is based on your area'southward median income. To be eligible for a USDA loan, you tin't exceed the median income past more than 15%. For instance, if the median salary in your metropolis is $65,000 per year, you could qualify for a USDA loan with a bacon of $74,750 or less. (15% of $65,000 = $9,750 → $65,000 + $9,750 = $74,750).

Is a USDA loan good?

A USDA loan is a slap-up pick for buyers with moderate or low income. It lets you purchase a house with nothing down and low mortgage rates — 2 huge benefits that simply one other loan program (the VA loan) offers. If your home is in an eligible area, it'south worth exploring a USDA-guaranteed loan. The chief drawback is that USDA loans require mortgage insurance for the life of the loan. So if yous can make a 20% down payment, you might prefer a conventional loan with no mortgage insurance payment.

Is USDA improve than FHA?

Both programs allow you buy with a depression down payment and crave mortgage insurance. USDA tin be used with zero down, just the habitation has to be in a qualified rural area, and the buyer has to meet income eligibility caps. FHA requires 3.v% down, simply there are no location or income restrictions. FHA also has more lenient credit requirements: You need a 580 credit score for FHA versus 640 for USDA). The correct loan type for you depends on where you're ownership and your financial situation.

How does the USDA loan work?

USDA loans are not straight loans from the regime. But they are backed by the U.Due south. Department of Agriculture, so they tin can offer downwardly payment assistance and low rates. Aside from that, USDA loans work like other mortgages. They're offered by mainstream lenders so you tin apply online, in person, or over the phone. And you however have to get pre-approved and authorize for a USDA loan based on your income, credit, debt, and other factors. One other difference is that the lender has to send the loan file to USDA to exist approved before underwriting. This tin can add effectually ii to three weeks to your loan processing fourth dimension.

Is there a minimum credit score for the USDA loan program?

On December ane, 2014, USDA implemented a minimum score of 640. Before that date, USDA set no minimum score for the program. All the same, most lenders did. When USDA implemented an official credit score minimum, it did non exclude very many additional buyers. If you are without a credit score, your lender may accept "alternating" tradelines to establish a credit history. (For case, on-time hire and utility payments that wouldn't typically be included in a credit study.)

What is the USDA programme'south minimum downwardly payment?

The USDA has no downward payment requirement. You lot tin finance 100% of the abode price with a USDA loan. However, if you do decide to make a down payment, you can lower your monthly mortgage payments and potentially beget a more than expensive home.

Are USDA mortgage rates good?

USDA loan rates are often lower than conventional 30-yr fixed mortgage rates. Plus, mortgage insurance rates are lower. This ways a USDA loan is often more than affordable overall than a comparable FHA or conventional loan.

When mortgage rates fall, tin can I refinance my USDA mortgage?

Aye, USDA loans are eligible for refinance into another USDA loan or a conforming conventional loan. The USDA Streamline Refinance Programme waives income and credit verification then closings tin can happen quickly. Home appraisals aren't required, either.

Tin can I do a cash-out refinance with the USDA program?

No, the USDA Rural Housing Plan is for abode ownership and rate-and-term refinances only.

Why does the USDA offer the Rural Development loan?

The USDA Rural Development loan is meant to aid moderate to low-income families go access to housing and mortgage loans in some of the less densely populated parts of the country. By enabling homeownership, the USDA helps create stable communities for households of all sizes.

What areas are eligible for a USDA loan?

With the USDA Rural Housing Program, your home must exist located in a rural area. However, the USDA's definition of "rural" is liberal. Many small-scale towns meet the "rural" requirements of the agency, as do suburbs and exurbs of many major U.S. cities. About 97% of the United states of america landmass fits the USDA loan's definition of "rural." Only 3% is ineligible at the fourth dimension of writing this article.

How can I discover if my area is USDA-eligible?

The website of the U.S. Department of Agriculture lists eligible USDA communities by Census tract. You are required to provide a home's exact address. The website will show whether that abode meets program guidelines.

Is in that location mortgage insurance (MI) on a USDA loan?

USDA loans crave mortgage insurance (MI) to be paid. This includes a 1.00% upfront guarantee fee, which is added to your loan residual at closing, and an annual fee of 0.35%, which is broken into 12 installments and added to your monthly mortgage payments.

Can I finance the Upfront Mortgage Insurance into my mortgage?

Yes, the USDA will allow you finance your Upfront Mortgage Insurance payment by adding it to your loan amount. For example, if you bought a new home for $100,000 and borrowed the full $100,000 from your lender, your Upfront Mortgage Insurance would be $1,000. You could and so increase your loan size to $101,000.

What's the maximum USDA mortgage loan size?

The USDA sets no loan limits. All the same, the corporeality you can borrow is limited by your income and your household's debt-to-income ratio. The USDA typically caps debt-to-income ratios to 41%. Even so, the program may be more lenient for borrowers with a credit score over 660 and stable employment, or who show a demonstrated ability to salve.

Is the USDA loan program limited to commencement-time buyers?

No, the USDA Rural Housing Plan can be used by first-time buyers and repeat buyers akin.

Where can I find a USDA loan lender?

The U.S. Department of Agriculture'southward website maintains a list of approved lenders for the Rural Housing Program.

What loan terms are available through USDA?

The USDA Rural Housing loan is available every bit a 30-yr stock-still-rate mortgage only. There is no fifteen-year fixed option, or adjustable-rate mortgage (ARM) program available via the USDA.

How much are the closing costs for a USDA mortgage?

Closing costs vary by lender and location. For example, some lenders take loftier origination charges. Others exercise not. The same is truthful for state and local governments. Costs are high in some states and depression in others. Because closing costs vary, be sure to shop effectually to find the about suitable combination of low mortgage rates and low costs.

Do I have to escrow my taxes and insurance with a USDA mortgage?

Yes, USDA mortgages require borrowers to escrow taxes and homeowners insurance with the lender. This means you'll pay your taxes and insurance along with your mortgage each month. You lot may not pay your real estate taxes or almanac homeowner insurance separately.

I can't beget closing costs. Tin I get a gift for my endmost costs?

Yep, USDA loans allow gifts from family unit members and non-family members. Let your loan officer know as shortly as possible that yous'll be using gifted funds, as this requires extra documentation and verification on the lender's role.

I negotiated to have the seller pay my closing costs. Is that allowed?

Yeah, the USDA Rural Housing Program allows sellers to pay endmost costs for buyers. This is known as "Seller Concessions." Seller concessions may include all or part of a buy's state and local government fees, lender costs, title charges, and any number of home and pest inspections.

Can I utilize the USDA loan for a vacation home?

No, the USDA loan cannot be used for a vacation home, information technology is for primary residences only.

Can I apply the USDA loan for an investment property?

No, the USDA loan cannot exist used for investment properties.

Tin I use the USDA loan programme for my working farm?

No, the Rural Housing Program is for residential belongings.

I recently went back to work. How long until I am USDA-eligible?

If you lot are a Westward-2 employee, yous are eligible for USDA financing immediately; y'all don't demand a job history. If you take less than two years in a job, however, you may not exist able to utilize your bonus income for qualification purposes.

I am self-employed. Can I apply the USDA loan program?

Yes, self-employed people tin apply the USDA Rural Housing Plan. If you are self-employed and want to use USDA financing, equally with FHA and conventional financing, you will be asked to provide two years of federal tax returns to verify your self-employment income.

Can I use the USDA loan program for a new construction home?

Yes, the USDA loan programme can be used for newly-built homes and other new structure.

Tin I use the USDA loan program to make repairs and improvements to an existing dwelling house?

Yes, the USDA loan plan tin can exist used to make eligible repairs and improvements to a dwelling house. This may include replacing windows or appliances; preparing a site with trees, walks, and driveways; drawing stock-still broadband service to the home; and, connecting water, sewer, electricity, and gas.

Can I use the USDA loan programme to make a home accessible to people with physical handicaps?

Yes, the USDA loan program tin can exist used to permanently install equipment to help household members with physical disabilities.

Can I utilize the USDA loan program to brand free energy-efficiency improvements to a habitation?

Yes, the USDA loan program can exist used to purchase and install materials meant to improve a dwelling's energy efficiency, including windows, covering, and solar panels.

Can a non-citizen qualify for a USDA loan?

Aye, along with U.S. citizens, legal permanent residents of the The states can besides utilise for a USDA loan.

Does income eligibility include household income?

Yep, a borrower'southward household income cannot exceed 115% of the expanse's median income.

Today's USDA mortgage rates

USDA mortgage interest rates are typically the everyman on the marketplace (next to VA loans).

Considering rates are already virtually tape lows, many home buyers who authorize for USDA can get incredible deals correct now.

To detect out whether you lot qualify for a USDA loan — and what your rate is — bank check with a lender.

Pop Articles

- Your Guide To 2015 U.S. Homeowner Tax Deductions & Revenue enhancement Credits Oct 8, 2015

- Minimum FHA Credit Score Requirement Falls 60 Points October 11, 2018

- Fannie Mae HomePath mortgage: low downwards payment, no appraisement needed, and no PMI January 23, 2016

- Fannie Mae'due south mandatory waiting period after bankruptcy, brusque sale, & pre-foreclosure is only two years Dec 11, 2018

- Gift letter for mortgage: How to give or receive a downwards payment gift Apr 8, 2021

- FHA Lowers Its Mortgage Insurance Premiums (MIP) For All New Loans January 26, 2015

- How to shop for a mortgage without hurting your credit score May vi, 2022

- Conventional Loan 3% Downwards Available Via Fannie Mae & Freddie Mac April viii, 2015

- three% Downwardly payment mortgages for first-time home buyers April 21, 2022

- Do bi-weekly mortgage programs pay your mortgage down faster? September 18, 2018

- Loan-to-value ratio for mortgage: LTV definition and examples March 17, 2022

- 2022 VA Loan Residual Income Guidelines For All 50 States And The District Of Columbia January 2, 2020

- 8 Ways To Get A Mortgage Canonical (And Not Mess It Up) May 26, 2016

- 4 ways to keep your mortgage closing costs low June 22, 2017

- USDA eligibility and income limits: 2022 USDA mortgage May 17, 2022

- Mortgage disbelieve points explained January xiii, 2022

- You Don't Need A 20% Downpayment To Buy A Dwelling February 20, 2019

- Beginning Time Dwelling Buyer : The Early-2017 Guide to Ownership a Home March 10, 2017

- Don't Have 20% To Put Downwardly? No Problem With These 5 Pop Mortgage Programs. March v, 2014

- USDA Home Loans : 100% Financing And Very Low Mortgage Rates April 18, 2017

- Buying A Domicile With A Boyfriend, Girlfriend, Partner, Or Friend July 17, 2016

The information independent on The Mortgage Reports website is for informational purposes only and is non an ad for products offered by Full Beaker. The views and opinions expressed herein are those of the author and do not reflect the policy or position of Full Chalice, its officers, parent, or affiliates.

Source: https://themortgagereports.com/14969/usda-loans-home-mortgage

Posted by: lamphearsuan1962.blogspot.com

0 Response to "Is Money Available For Usda Loans Nov 2018 Cr"

Post a Comment